Stock Market Jitters Part II

The recent stock market drops are creating jitters for millions of investors. With concerns around rising interest rates, trade policies and higher inflation now is the time to analyze your investment risk. Risk can be defined as possibility of loss or injury. Regarding investing, risk can be defined as the chance an investment’s actual return will differ from the expected return. Risk includes the possibility of losing some or all of the original investment. Risk is also the potential to lose money permanently. Those statements regarding risk are enough to conjure the feeling that I could end up with less money than I started with and less than I need in the long-term. Although we know the definition and perils of risk, many retirees and pre-retirees are making the mistake of taking on too much investment risk.

One of the most basic principles of investing is to gradually reduce your risk as you get older, since retirees don’t have the luxury of waiting for the market to bounce back after a dip. The dilemma is figuring out exactly how safe you should be relative to your stage in life. The solution to that dilemma is found in two strategies. I discussed the first strategy last week, now I will discuss the second strategy.

The second strategy to the dilemma of determining how you should invest your retirement dollars is understanding the difference between returns and volatility.

Let’s say you were given the choice to invest in two funds, Fund A or Fund B and the only data you have on either fund is that for the last 15 years (2000-2015) Fund A has averaged 5.66% per year with a Sharpe Ratio of 1.91% and Fund B has averaged 5.65% per year with a Sharpe Ratio of 0.21%. Which fund would you invest in? Probably not enough information to make an informed decision right? What if I told you that Fund A was a well-known index fund and Fund B was a lesser known fund, which would you choose? More than likely you would choose the well-known index fund. But how do we know which fund performs better for our particular goals and objectives? We will answer this question from three hypothetical illustrations/scenarios.

First scenario, let’s assume you invested $1,000,000 in Fund A starting in the year 2000 and $1,000,000 in Fund B starting in the same year 2000. We will assume no additional funds were deposited nor were funds withdrawn from either account. As of 12/31/2015, which Fund would you assume has the higher value Fund A or Fund B. As of 12/31/2015 Fund B has a ending value $86,000 higher than Fund A. Now what made the $86,000 difference in Fund B compared to Fund A? Was it the commutative property of mathematics that says numbers in any order yield the same result? No, the difference is returns versus volatility. Let us go deeper in our understanding of the mistake of taking on too much risk.

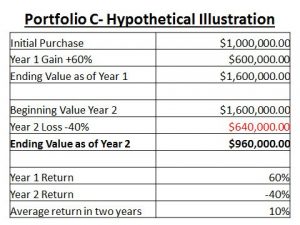

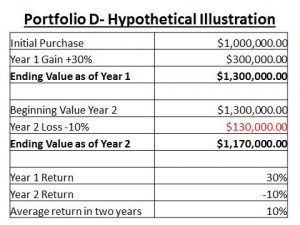

Second scenario, let’s assume you purchased $1,000,000 worth of stock in another portfolio we will call Portfolio C and $1,000,000 worth of a stock in another portfolio we will call Portfolio D and you plan on investing in these two portfolios for only two years. How might volatility effect both Portfolio C & D?

Well let’s assume, Portfolio C made 60% in Year 1 with a gain to your portfolio of $600,000 bringing your total after Year 1 in Portfolio C to $1,600,000. In Year 2, let’s also assume it lost a -40% reducing your value by (-$640,000) which brings your ending value down to $960,000 at the end of Year 2 with an average return of 10%.

Now let us assume Portfolio D made 30% in Year 1 with a gain to your portfolio of $300,000 bringing your value after Year 1 in Portfolio D to $1,300,000. In Year 2, let us assume the portfolio lost a -10% reducing your Portfolio value by (-$130,000) which brings your value down at the end of Year 2 to $1,170,000. Both portfolios averaged the same 10% return after Year 2, but Portfolio D had a higher ending value. With that being said, if you would prefer to have results of Portfolio D, this shows us you can live with low returns but you cannot live with big losses.

Finally, let’s return to our first two portfolios, Portfolio A and B. What would happen if you invested $1,000,000 in each portfolio and started receiving income of $50,000 per year from each Portfolio from 2000-2015, which account would have a higher account value 15 years later? According to our hypothetical illustrations Portfolio B does, but how? From this simple concept, that volatility trumps returns. A low volatility discipline maybe the difference between retirement success or retirement failure.

Before I offered these three scenarios, we could have determined which account would fit your overall objective better by analyzing the Sharpe ratios. A lower Sharpe ratio indicates the probability of a portfolio providing lower volatility in a turbulent market cycle.

Remember the key to retirement income success is living with the smaller gains instead of living with the bigger losses. Since we learned from our hypothetical illustrations that volatility trumps returns every time, do not make the investment mistake of taking on too much investment risk.

If you would like to know if you are taking too much investment risk or how much investment risk you are currently taking feel free to contact our office at 615-678-6603 for a complimentary risk analysis.